Yole Développement Concludes: “Independent Phosphor Companies Free the Market from IP Blocking by Market Leaders”

Phosphors are a keystone of LED technologies, enabling the conversion of the monochromatic blue or near-UV light emitted by LED chips into a richer spectrum of color approaching or exceeding that of other artificial light sources. Yole Développement announces today its new report “LED phosphors” which provides a detailed description of the LED phosphor industry.

- (Source: LED Phosphors report, Yole Développement, October 2012)")

This report includes an extensive list of manufacturers, an analysis of established and emerging composition and deposition methods, and detailed quantifications. It also provides an analysis of major technology trends like the emergence of remote phosphor and Quantum Dots.

Finally, due to its potential impact on the LED phosphor industry, the Rare Earth supply crisis and future supply and demand trends are analyzed in detail, with an emphasis on the elements that are critical for the fluorescent and LED lighting industries.

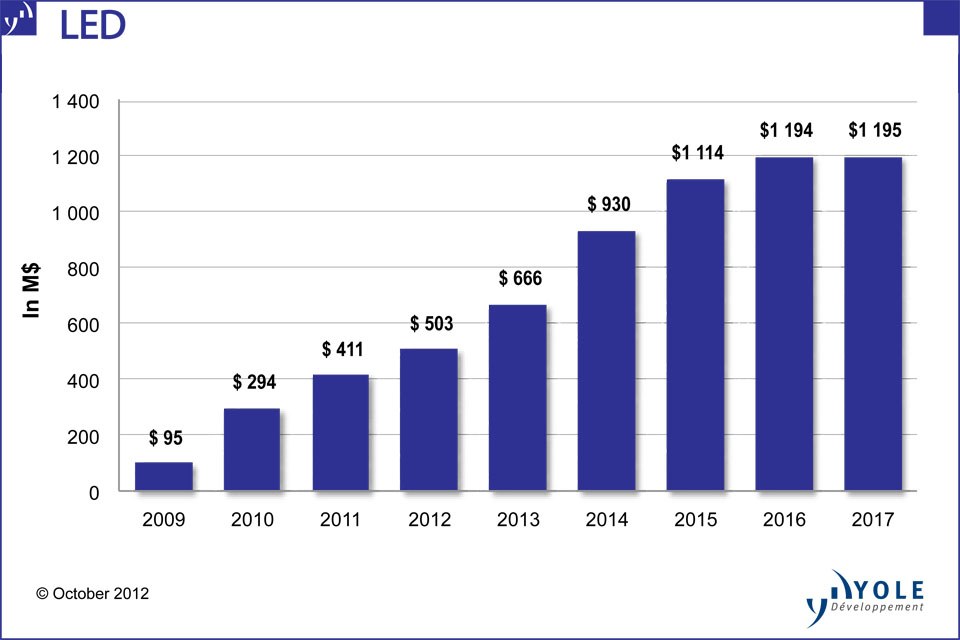

“LED phosphor market to more than double in the next five years”, announced Yole Développement:

At the dawn of the HB LED industry in the early 2000’s, the bulk of the LED phosphor industry was under the control of the major LED players that held key IP in the various domains, and selectively granted licenses and cross-licenses. “The landscape changed in the mid 2000’s with the emergence of phosphors that were “IP-free” credible alternatives to YAG and TAG, commercialized on the open market by independent phosphor manufacturers unaffiliated with LED manufacturers”, explains Dr Eric Virey, Senior Analyst, LED at Yole Développement.

This report provides a detailed list of more than 50 companies that are involved in LED phosphor manufacturing. “More than 20 of them are located in China, where we’re observing the emergence of vendors with improving quality and potentially credible IP to satisfy the tier-one Chinese LED makers that have world class ambitions and who favor IP and performance vs. price”, adds Dr Eric Virey.

Overall, Yole Développement expects the phosphor market to grow significantly during the next five years, and potentially pass the $1 billion mark by the end of this period. However, a significant fraction of this market will remain captive. Yole Développement’s report provides average selling price trends and detailed forecasts by phosphor type and composition.

Technology is still a key opportunity for differentiation in order to increase performance and design in the face of a strong and limiting IP:

The combination of YAG phosphor + blue LED remains the solution of choice for applications where high CRI and warm color temperature are not required, but Nichia’s strong IP limits access to YAG to selected partners and major LED manufacturers that have been able to negotiate cross-license agreements thanks to their own strong IP position. While still not on an equal footing with YAG in terms of performance, Silicates have improved significantly and are closing the gap. However, as Nichia’s critical IP is set to expire in the next few years, an increasing number of phosphor manufacturers are offering YAG compositions as well.

The next battle in the LED phosphor industry stems from the rapid growth of LED applications that require warm colors and saturated reds in display or residential and retail lighting. For these, additional red and/or green phosphors are added to the mix. Nitrides and Oxynitrides offer excellent performance but are both controlled by Denka and Mitsubishi Chemicals, with strong IP obtained from NIMS. Market price for these materials is 5x to 10x higher than that of yellow phosphors. Multiple organizations are therefore scrambling to develop better, cheaper and non IP-restricted compositions. Tungstates, molybdates, carbidonitrides, Green Aluminates and Selenides are being investigated. In addition, Quantum Dots are finally emerging as a credible alternative to traditional phosphor in some applications. “But phosphor composition is not the only key factor. Manufacturing technology, deposition methods and system design all have significant impact on LED and overall system cost and performance”, explains Dr Eric Virey. This report provides a detailed list of established and emerging compositions and deposition technologies.

Remote phosphors could present a significant upside:

Remote phosphors offer significant benefits in terms of system performance and efficiency. However, they increase the required amount of phosphor material and associated cost by orders of magnitude. This constitutes the major roadblock for adoption. With some applications though, remote phosphors are the best option for reaching the required performance, and the additional phosphor cost can be partially or completely offset at the system level by improving its overall performance and reducing component count.

The adoption of remote phosphors is decided on a case-by-case basis depending on the application, performance and cost targets.

A rare earth shortage could impact the LED industry in the mid-term:

While supply constraints on light rare earth should ease soon, tension will persist for the heavier elements, including Yttrium, Terbium and Europium, which are critical to both fluorescent lamp and LED makers. Shortages could appear and persist even after 2015. Fluorescent lamp is the major application competing with LED for these resources. In the short-term, as incandescent and other inefficient light sources are phased out of the market in most countries, the consumption of fluorescent lamps will increase significantly, putting additional strain on supply.

The Author:

Dr Eric Virey, holds a Ph-D in Optoelectronics from the National Polytechnic Institute of Grenoble. In

the last 12 years, he’s held various R&D, engineering, manufacturing and marketing position with

Saint-Gobain Crystals, in charge of Sapphire substrates and materials for optical telecoms. Eric has

authored multiple reports for Yole Développement, including Sapphire 2010 and 2011, LED Packaging

2011, Status of the LED Industry, LED Mantech, II-V Epitaxy, and LED Front-End Manufacturing.

Catalogue price:

Euros 3,990.00 (single user license) - Publication date: October. 2012.

For special offers and the price in dollars, please contact David Jourdan (jourdan@yole.fr or +33 472

83 01 90).

Companies cited in the report:

Alkane Ressource, Aratura, Asian Rare Earth, Aurora Energie Corp, Avago, Avalon Metal, Beijing Nakamura Yuji Science and Technology, Chi Mei Opto, China Glaze, Citizen Electronics, Cree, Daeioo Electronic Materials, Dalian Luming, Denka, Disco, Dominant, Dott Technology, Dow Electronic Materials, Eastman Kodak, Edison Opto, Essemtec, Everlight, Evident Technology, Force 4, GE, Global Tungsten, Great Western Mineral Group, Greenland Minerals & Energy, Grirem, Hangzhou Daming Phosphor Material, Hano-Li, Harvatek, Horner APG, Hsiung-Din, Hung-Ta, Intematix, Irico, Iswell , Jiangmen KanHoo Industry (Keheng), Jiangnan Phosphor, Jiangsu Bree Optronics, Jingneng, KAIST, KRICT, Kumho Electric, Ledzworld Technology, Leuchtstoffwerk (LWB), Lextar, LG, Light Prescription Innovators (LPI), Lightscape, Lite On, Litec, Lorad Chemical, Lucimea, Lumimicro, Lumisand, Lynas, Mason, Merck, Mesolight, Mitsubishi Chemicals, Molycorp, Mujin, Nanoco, Nanosys, Nemoto, Neo Material Technolog

For more information or to order the report please visit http://www.i-micronews.com/reports/LED-Phosphors/14/320/

About Yole Developpement:

Beginning in 1998 with Yole Développement, we have grown to become a group of companies providing market research, technology analysis, strategy consulting, media in addition to finance services. With a solid focus on emerging applications using silicon and/or micro manufacturing, Yole Développement group has expanded to include more than 50 associates worldwide covering MEMS, Microfluidics & Medical, Advanced Packaging, Compound Semiconductors, Power Electronics, LED, and Photovoltaics. The group supports companies, investors and R&D organizations worldwide to help them understand markets and follow technology trends to develop their business. – www.yole.fr