Packaged LED Market Report from Yole Développement & EPIC Forecasts Tremendous Growth between 2012 and 2018

Yole Développement and EPIC announce their report dedicated to the LED industry: “Status of the LED Industry”. The report presents all applications of LEDs and associated market metrics, LED cost reduction opportunities, entire LED value chain, a deep analysis of the general lighting application and an analysis of geographical trends.

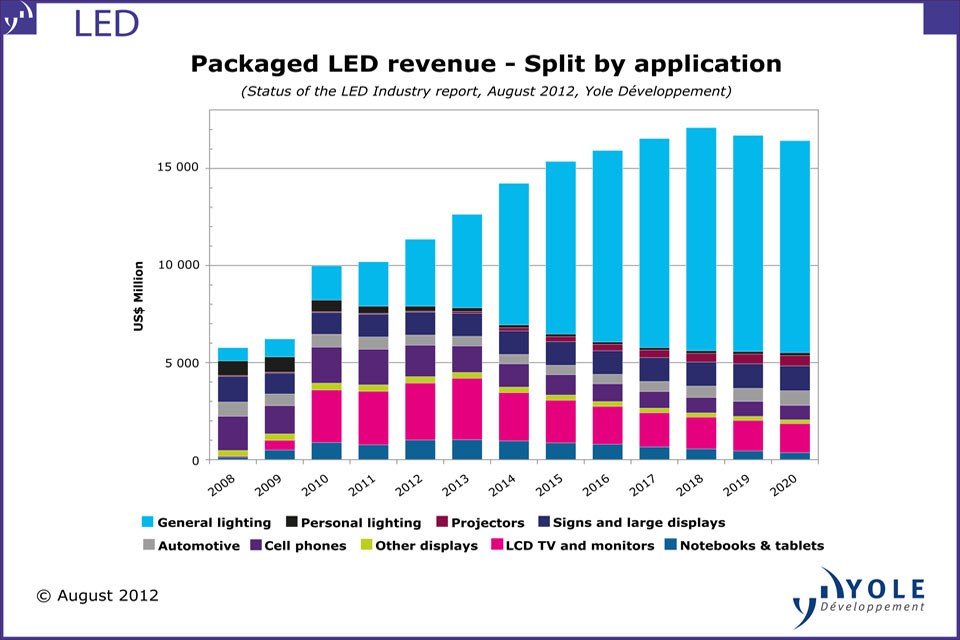

The LED industry is entering its third growth cycle: general lighting

Growth of the LED industry has come initially from the small display application and has been driven forward by the LCD display application. LED TV was expected to be the LED industry driver for 2011 but the reality was quite different… Lower adoption of LEDs in the TV market and the entry of several new players, mostly from Asia, created a climate of overcapacity, price pressure and strong competition. As a consequence, packaged LED volume was about 30% lower than expected and revenue shrank due to strong ASP pressure.

“In 2012, most companies have moved to the new “El Dorado” of LED business: general lighting, which represents the next killer application for LEDs. But enabling massive adoption of the technology for such an application still requires a large decrease in the cost of LED-based products…,” explains Pars Mukish, Market and Technology Analyst, LED at Yole Développement.

Yole Développement and EPIC estimate packaged LED revenue will reach a market size of $11.4B in 2012 and will peak to $17.1B by 2018. Growth will be driven both by the display (LCD TV) and general lighting applications until massive adoption of LEDs in lighting. From 2014, the third growth cycle of the LED business will accelerate with the general lighting application representing more than 50% of the overall packaged LED business. In terms of volume, LED die surface will increase from 22.5B mm² (2012) to 80B mm² (2018). This will prompt substrate volume growth from 8M x 2” equivalent (TIE) in 2011 to 39.5M x 2” equivalent in 2018 with a CAGR of 26%.

Yole Développement & EPIC analysis presents all applications of LEDs and associated market metrics within the period 2008-2020, detailing for each application: drivers & challenges, associated volume and market size (packaged LED, LED die surface), penetration rate of LEDs…

Cost of packaged LEDs still needs to be reduced by a factor x10 to enable massive adoption in general lighting

The adoption of LEDs for general lighting applications strongly depends on technology and manufacturing improvements. This is required to drive performance and cost of LED solutions to a trigger point where massive adoption could start. Industry consensus points out a cost reduction per lumen of packaged LEDs by a factor x10. This can be achieved through a combination of manufacturing efficiency and performance improvement, such as:

• Access to larger size wafers

• Improvements in LED epitaxy cost of ownership through yield and throughput

• Improved packaging technologies (phosphors, optics…)

• …

Additionally, improved package and luminaire design will also enable significant cost reduction (“design for manufacturability”).

In this technology & market analysis, our experts analyzed LED cost reduction opportunities, detailing: cost structure of packaged LEDs (and LED-based lighting products), key technologies and research areas…

China’s GaN MOCVD reactor capacity has increased by a factor x20 the last 3 years

The capacity for GaN LED epitaxy has increased dramatically in 2010 and 2011. This increase took place across all regions but was most dramatic in China (increased by a factor x20 of the reactor capacity between Q4 2009 and Q1 2012).

“Most emerging Chinese LED epiwafer and die manufacturers are still lagging significantly behind their competitors in term of technology maturity and LED performance,” says Dr Eric Virey, Senior Analyst, LED at Yole Développement.

The bulk of those new companies are not yet capable of manufacturing LEDs to address the large display and general lighting applications that are currently driving the market. In the mid-term, consolidation of the Chinese LED industry will occur (scenario in the central government’s new five-year plan), and China should became a major actor in the LED industry.

The report presents LED value chain, detailing: reactor capacity by region with an analysis of capacity vs. demand, actors involved with a focus on leading LED epitaxy and packaging companies (2011 ranking by revenue)…

New business models are mandatory to capture added value of LED lighting

Ultimately, the long life of Solid State Lighting (SSL) technology will totally change the lighting market by dramatically increasing the length of the replacement cycles. The replacement market (aftermarket) will be strongly impacted, pushing traditional players of the lighting industry to define new strategies to capture profit (intelligent lighting, lighting solutions…).

“In addition, as value is moving to the top of the value chain (module and luminaire levels), several players that were originally involved only at LED device levels will develop strategies of vertical integration in order to capture more value,” added Tom Pearsall, General Secretary, EPIC.

But accessing distribution channels represents a big challenge for those players who develop new approaches to sell their lighting products (e-commerce, new distributors….). The rise of LED lighting will therefore depend on the right merger of the emerging LED industry with the traditional lighting industry.

The report presents a deep analysis of the general lighting application, detailing for each market segment: status & trends, drivers & challenges, regulations & standards, market metrics… An analysis of geographical trends is also developed.

About the report “Status of the LED Industry”

• Authors:

Pars Mukish works at Yole Développement as a Market and Technology Analyst in the field of LED. He holds a master degree in Materials Science and a master degree in Innovation & Technology Management (EM Lyon - France). In the past, he has worked as Marketing and Techno-Economic Analyst at the CEA.

Dr Eric Virey, holds a Ph-D in Optoelectronics from the National Polytechnic Institute of Grenoble. In the last 12 years, he’s held various R&D, engineering, manufacturing and marketing position with Saint-Gobain Crystals.

Tom Pearsall, General Secretary, EPIC. In 2003, Tom started the European Photonics Industry Consortium. Before EPIC, he works among others for Bell Laboratories, Thomson/CSF and Corning. He is a Fellow of the American Physical Society and a Fellow of the IEEE.

• Catalogue price:

Euros 3,990.00 (single user license) - Publication date: August 2012.

For special offers and the price in dollars, please contact David Jourdan (jourdan@yole.fr or +33 472 83 01 90).

• Companies cited in the report:

A-Bright, Advanced Photonics, American Bright, American Opto Plus, AOT, ApexScience & Engineering, APT Eelctronics, Aqualite Co, Arima, AUO, Avago, Bridgelux, Bright LED, Brightview electronic, CDT, Century Epitech, Chi Mei Lighting Technology, Citizen Electronics, CREE, CS Bright, Daina, Dominant Semiconductors, Edison, Elec-tech, Enfis, Epiled, Epilight Technology, Epistar, EpiValley, Everlight, Excellence Opto, Fangda group, Formosa epitaxy (Forepi), Galaxia Photonic, GE, Genesis Photonics, Golden Valley Optoelectronics, Hangzhou Silan Azure, Harvatech, HC SemiTek, Heesung, High Power Opto, Hi-Light, Hueyjann Huga, Huiyuan Optoelectronic, Hunan HuaLei Optoelectronic, Hunin Electronic, Idemitsu Kosan, Illumitex, Invenlux, Itswell, KingBright, Kodenshi, Konica Minolta, Korea Photonics Technology Institute (KOPTI), Kwality group, Lattice Power Corporation, LedEngin, LEDTech, Lemnis, Lextar/Lighthouse, LG Display, LG Innotek, Lighting Science, Ligitek, Lite-On, LongDeXin (LDX), Lumei Optoelectronics, Lumenmax, Lumex, Lumileds, LumiMicro, Lumination, Luminus, Lumitek, Lustrous Technology, Luxpia, LuxtalTek, MokSan Electronics, Moser Baer, Nanosys, Nanya, Nationstar, Neo-Neon, Nichia, NiNEX, Oasis, Optek Technology, Opto Tech, Osram, ParaLight, Philips, Power Opto, Powerlightec, Rainbow Optoelectronics, Rohm, Samsung SEMCO, Sanan Optoelectronics, Sanken Electric, Seiwa Electric, SemiLEDs, Seoul semi / Optodevice, Shandong Huaguang Optoelectronics, Sharp, Shenzen Mason Technology, Shenzen Mimgxue, Shenzen Yiliu Electronic, Shenzhen Refond, Showa Denko, Stanley Electric, Sunpu Opto, Supernova, Sylvania, Tekcore, TESS, Tonghui Electronic Corporation, Toshiba, Toyoda Gosei, TSMC, Tyntek, UDC, Unity Opto, Visera Tech, Vishay, VPEC, Walsin Lihwa, Wellipower, Wenrun Optoelectronic, Wooree LED, Xiamen Changelight, Xiamen Hualian, Ya Hsin, Yangzhou Huaxia Integrated Photoelectric (DarewinChip), Yangzhou Zhongke Semiconductor, YoungTeck, Yuti Lighting Shanghai, Zoomview (Xi An Zoomlight)…

This list is not exhaustive. The full list will be available soon on our website I-Micronews.com, Reports section.

About Yole Développement:

Beginning in 1998 with Yole Développement, we have grown to become a group of companies providing market research, technology analysis, strategy consulting, media in addition to finance services. With a solid focus on emerging applications using silicon and/or micro manufacturing, Yole Développement group has expanded to include more than 50 associates worldwide covering MEMS, Microfluidics & Medical, Advanced Packaging, Compound Semiconductors, Power Electronics, LED, and Photovoltaic. The group supports companies, investors and R&D organizations worldwide to help them understand markets and follow technology trends to develop their business. For more information, please visit our website: www.yole.fr

Contact: Sandrine Leroy (leroy@yole.fr) – Phone: +33 (0) 472 83 01 80

About EPIC:

The European Photonics Industry Consortium, EPIC, has three important activities: dialogue with the European Commission, ownership of the European roadmap for photonic technologies, and developing the critical human resource of trained scientists and engineers in the European economic area. EPIC organises and runs European workshops on photonics technologies.

EPIC is composed of 80 member organizations and over 400 associate members. The strength and influence of EPIC throughout Europe comes from getting its members to work together. EPIC members played the leading role in creating the Photonics21 platform. For more information: www.epic-assoc.com

Contact: Martine Keim-Paray (keim-paray@epic-assoc.com ) – Phone: + 33 (0) 1 4505 7263