IDTechEx Compares OLED vs. LED Lighting - Is there room for OLED Lighting

Dr Norman Bardsley, Bardsley Consulting & Dr Khasha Ghaffarzadeh, Senior Technology Analyst at IDTechEx Research find that in its “most likely” forecasts scenario OLED lighting will become a $1.3 billion market in 2023 – equating to 1.3% of the market size of LED lighting at that time.

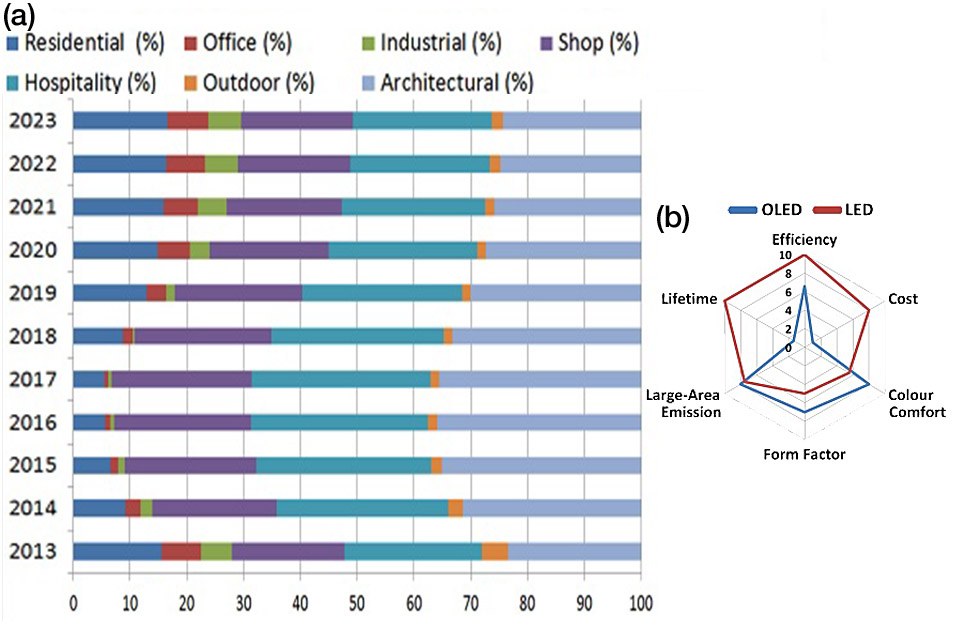

![The relative monetary contribution of each lighting market segment to the total OLED market 2013-2023 (a), radar chart comparing attributes of OLED and LED lighting (b) [Source: IDTech]](https://www.led-professional.com/media/business_reports_idtechex-compares-oled-vs.-led-lighting-is-there-room-for-oled-lighting_relative%20monetary%20contribution%20of%20each%20lighting%20market%20segment%20to%20the%20total%20OLED%20market%202013-2023.jpg/@@images/image-1280-d79c1008d66a8dd4b99921220f7cc916.jpeg "The relative monetary contribution of each lighting market segment to the total OLED market 2013-2023 (a), radar chart comparing attributes of OLED and LED lighting (b) [Source: IDTech]")

The new report by IDTechEx “OLED vs LED Lighting 2013-2023” (www.IDTechEx.com/oled) finds that OLED lighting is likely to struggle to define and communicate its unique selling points and may remain an over-priced and under-performing option compared to LED lighting, unless Apple-like design innovation occurs. OLED lighting companies will inevitably have to capitalise on superior design features to carve out niche markets in the hospitality, shopping and architectural sectors. Profits for panel makers will be squeezed due to stiff competition and value will migrate downstream to fixture/luminaire designers, who will be the demand creators.

OLED lighting performance today - efficiency and lifetime

OLED displays are growing quickly but their lighting counterparts are still actively trying to define their unique selling points vis-à-vis LED lighting. Today, they lag behind in terms of efficiency. This is because LEDs regularly offer 90-100 lm/W at package level (the LED chip encapsulated), while OLED modules are still in the region of 20-50lm/W. The lifetime of LEDs far exceed that of OLEDs. Indeed, LED lamps regularly offer in excess of 50,000 hours, which is why they initially found a niche market in out-of-reach outdoor applications. In contrast, OLED lighting offers 5,000 to 15,000 hours of operational life even when encapsulated.

Costs:

LED lighting is also now low cost, selling at $5/klm at package level (luminaires costs $20-$100/klm). Contrast this with the extortionate price of OLED today. They cost $300-$500/klm at panel level, excluding the cost of fixture design, retail, installation and profit margins. The main cost drivers are the encapsulation layer (barrier, adhesive and desiccant) and integrated substrates (transparent conductive layer, substrate and out-coupling layer).

In the current configuration, cavity glass is used as the barrier. This is expensive because (a) additional processing is required (sand blasting) to carve out a cavity, and (b) large glass manufacturers are reluctant to commit production capacity given the low demand. A change in system configuration from, first, cavity to frit glass and, second, from frit glass to thin film encapsulation is needed to drive the cost down. Today, encapsulation layers (including desiccant and adhesive) cost $400-$500/m2.

The integrated substrate is also a substantial cost driver. The integrated substrate includes the substrate (glass), transparent conductive layer (mostly ITO), metal electrodes, planarization (all patterned by photolithography/etch) and external light extraction film. The entire stack today costs $800-$900/m2 although this can be driven down to $100-$120/m2 in 2023. Innovation is taking place here with the advent of printing, grid materials, etc.

The situation is summarised below for the performance of OLED and LED lighting today.

OLED lighting offers high potential for large-area emission, although today OLED production takes place on Gen-2 substrates only. Similarly, OLED lighting offers good form factors, although today most OLED lighting applications are made on rigid glass.

Nevertheless, OLED lighting is still embryonic:

It is of course important to add that LED lighting development is far more mature – and more money has been spent on it than OLED lighting. Recently many companies have become active in OLED lighting and investment is increasing. For example, we expect the active materials to experience a fast cost reduction rate. This is because of leverage from the OLED display industry and also because costs will scale with volume. This is different from the other two layers since the demand is mostly driven by factors outside the OLED lighting space. Currently, active materials cost $350-$400/m2 but expect this to fall to $70-$90/m2 in 2023.

The growth of the OLED display industry will aid the OLED lighting sector with cheaper, higher performance devices over time – with some overlap in supply chains. The challenges faced in OLED lighting applications will not be solved by the panel manufacturers alone.

Design factors:

LED lighting is intrinsically a point source light, whereas OLED lighting is a surface emission device. While OLED lighting is likely to have a competitive edge here, its advantage is not as compelling as first evident. This is because the use of multiple LEDs in conjunction with waveguides is enabling the effective realisation of surface emission. At the same time, most OLED production today takes place on Gen-2 substrates.

Form factor (mechanical flexibility) is often claimed as a major selling point too. Today OLED technology falls short due to the encapsulation layers being based on glass – but progress on flexible barriers for OLED displays is likely to help this in the future. OLEDs also have the edge on colour warmth, low weight and thinness.

The onus over the coming years is therefore likely to be on luminaire/fixture designers who develop and sell niche products, capitalising on improved design parameters made available by OLEDs.

Markets:

The report from IDTechEx (“OLED vs LED Lighting” www.IDTechEx.com/oled) offers a broad yet detailed overview of both LED and OLED lighting, going through fabrication processes, material compositions, technology roadmaps, and key players. The device attributes of each technology are also critically assessed, examining parameters such as colour warmth and controllability, flexibility, efficiency, surface emission, lifetime, wafer size, and luminaire design.

This report also offers a blunt market assessment. Detailed cost projection roadmaps are developed, factoring in estimated cost evolution of the integrated substrates, encapsulation layers and materials. Changes in system configuration and material composition required to enable the cost roadmaps are outlined. We also factor in production costs including capital and labour. Values are expressed in units of $/unit and $/klm. A summary of the relative contribution of each lighting market segment to the total OLED market between 2013 and 2023 is shown in the figures.

Based on our “most likely” scenario, IDTechEx forecast the market will grow to $1.3 billion in 2023 and initially grow at a rapid rate of 40-50% annually, although the initial market base in very small. We contextualize our assessment by expressing our market forecast in units of equivalent 60W incandescent bulbs. We assess the implications of our market forecast for the global capital investment and production capacity. We compare the market size to that of LEDs (including automotive, backplane and residential) at module level. Production capacities are compared too to further set out forecasts in prospective. Our methodology is clearly laid out in the report, as are all our underlying assumptions.

For more details please see www.IDTechEx.com/oled.

About IDTechEx:

IDTechEx guides your strategic business decisions through its Research and Events services, helping you profit from emerging technologies. We provide independent research, business intelligence and advice to companies across the value chain based on our core research activities and methodologies providing data sought by business leaders, strategists and emerging technology scouts to aid their business decisions. To discuss your needs please contact us on research@IDTechEx.com or see www.IDTechEx.com.